The true impact of COVID-19 on the restaurant industry - survey results

To better understand the impact of the COVID-19 outbreak on restaurants, JLL, in partnership with MERA (Middle East Restaurant Association) and GRIF (Global Restaurant Investment Forum) launched a survey in the beginning of April 2020 to quantify the effects of COVID-19 on the restaurant industry.

The outbreak of COVID-19 has had immediate impact on the Food and Beverage (F&B) industry, with strict lockdown measures resulting in restaurant closures and a switch to online delivery platforms. Even with measures easing in some cities across the Middle East, allowing for a 30% occupancy, consumer hesitation has meant footfall remains low.

To better understand the impact this has had on restaurants, JLL, in partnership with MERA (Middle East Restaurant Association) and GRIF (Global Restaurant Investment Forum) launched a survey in the beginning of April 2020 to quantify the effects of COVID-19 on the restaurant industry.

Over the month of April, we have collected responses from 250 respondents representing over 1,800 restaurant units across the world. 70% of our responses came from the Middle East and 25% from Europe.

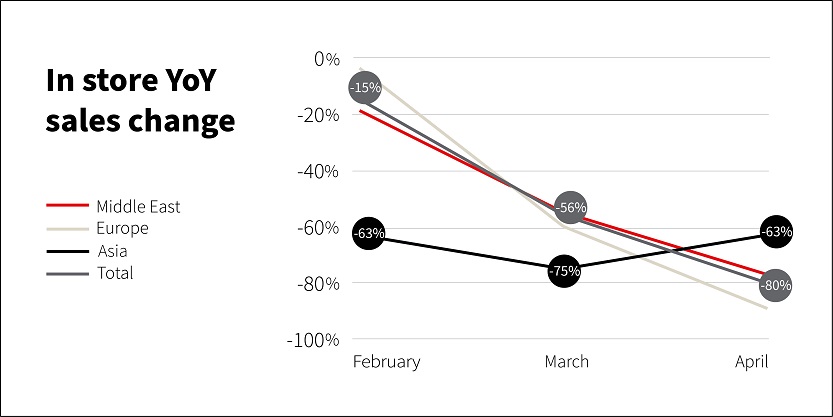

In-Store Sales

As expected, we see a sharp decline of in-store sales in the Middle East and Europe, due to both curfew measures and consumer hesitation to expose themselves to any health risk.

In the Middle East, restaurateurs experienced an annual decline in in-store sales of -19% and -55% for the months of February and March respectively. Expectations were for a -77% drop during the month of April.

In Europe, respondents have indicated that February in-store sales drop by -4% and a then by a more drastic -60% in March, reflecting the time at which measures were imposed, and their severity. Restaurateurs in Europe however, expect April in-store sales to drop -89% on an annual basis. This indicates respondents in Europe are more bearish than their Middle East counterparts. Despite the limited response rate in China, we have included these in the analysis above as they portray more of an optimistic outlook for April, reflecting a slight recovery post-easing lockdown measures.

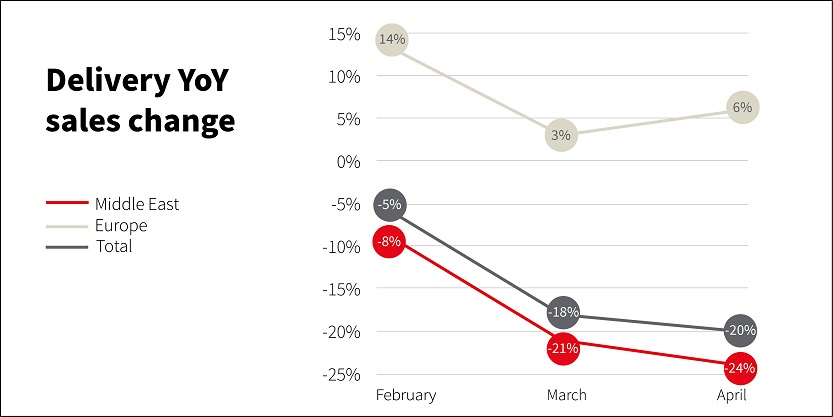

Delivery Sales

Based on the results of our survey, we find that 14% of operators in the Middle East introduced delivery due to Covid-19. Delivery sales have decreased in the Middle East over the period, compared to 2019. On average, the decline noted was -8% in February and -21% in March, with a -24% expected in April. This decline can be attributed to the already well-established delivery business in the Middle East, which was impacted heavily as work-from-home saw people opt for eating in as opposed to ordering food which would have been the case if they were in the office.

By contrast, 20% of operators have introduced delivery services in Europe due to the pandemic. However, sales in Europe saw a 14% increase in February and a 3% increase in March. Expectations are for a further 6% increase in delivery-sales in April. This reflects the more active switch to online food delivery services during the pandemic across Europe.

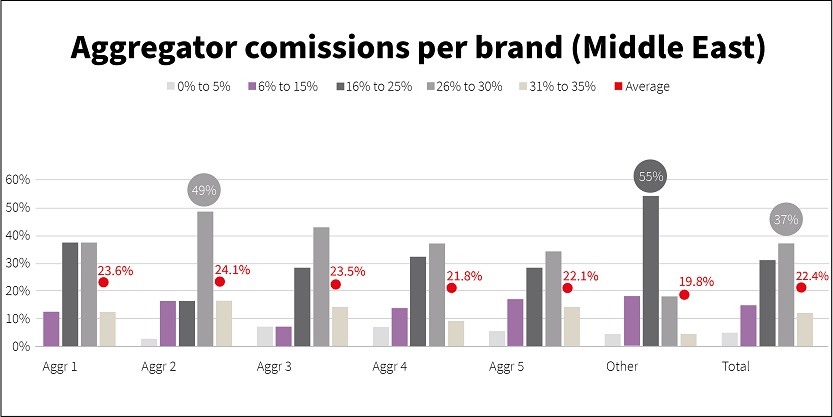

Aggregator Commissions

Aggregator commissions are those fees charged by online delivery-services platforms. In the Middle East and Europe, an average of 93% of restaurants subscribe to these services which typically come at a higher price, usually set as a commission to sales.

In the Middle East, we find 32% of the aggregators charge between 16% and 25% of sales, and 36% charge between 26% and 30% of sales. In Europe, prices are on average 5.7% higher and in Saudi Arabia, 3.5% lower than the Middle East. Despite the various benefits these aggregators bring, fees are relatively high potentially making delivery unprofitable for businesses. In the Middle East, although many aggregators have provided support during COVID-19, by lowering fees or commissions, we find the restaurant industry looking for ways to move away from this business model by offering in-house delivery, or coming together with other outlets to create their own aggregator with lower fees.

Landlord Support

At the time of our survey and in addition to the fiscal and monetary policy responses on behalf of governments we found that 41% of respondents in Europe had received landlord support, compared with 36% in the Middle East. Across the responses, landlord support came in three main forms:

- Rent Free: The landlord forgoes rent completely for a period of 1 to 3 months.

- Rent Holidays: 1 to 3 months’ rent was deferred to the end of the lease. In some instances, this was offered for the duration of the lockdown.

- Rent Discount: A deduction of rent from 35% to 75% was offered to the occupier.

How long can the industry survive?

The rate and severity of measures, and the variance in impact based on social isolation and policy responses will determine the recovery profile of the F&B industry. Based on sentiment however, 38% of the industry globally (Middle East included), expect annual sales to drop between -41% and -60% compared to projections set at the start of the year. Another 24% expect the situation to be worse, with their projections showing a decrease of up to -80%. Having said that, the sentiment in Europe is more positive than that in the Middle East, given government support and the cash position of some operators.

Coming back to life?

While it is difficult to assess when the situation will ease, it is imperative that various entities, both public and private, come together to create innovative solutions for the F&B industry post COVID-19. Some considerations we recommend:

- Landlords and tenants need to collaborate and work closer with one another to come out of this successfully. Having said that, both their demands need to be met to ensure survival.

- Non-negotiable rents and lease terminations will create voids that will be difficult to fill in the future.

- The restaurant business has an extremely low cash turnover timing. No sales equals no cash to pay rents, suppliers or employees, and hence support is needed at all levels of the operation.

- We believe the fairest approach moving forward is turnover rents. This alleviates “fixed” costs to operators but also aligns benefits for landlords as business picks back up.

- It will take some tenants up to 18 months to get back to historic turnover levels. Many will need support for much longer than curfew or lockdown periods.

- While both landlords and tenants may want to make portfolio-wide decisions, the reality is that some stores will be affected disproportionally by COVID-19. Therefore, working on a case-by-case basis on how to consider each store will net more positive outcomes

Finally, as we have seen during many crisis, difficult times fuel creativity. Like many successful companies we’ve seen emerging in crisis, we expect innovative and disruptive concepts to stem as a result of stronger collaborative practices.

For more information on this survey or our Foodservice Consulting Services, please reach out to Alexis Marcoux-Varvatsoulis, Foodservice Consulting Lead MENA on alexis.mv@eu.jll.com